5 Tax and Structures

Partnership taxation

A partnership doesn't pay tax directly.

Instead, it distributes its net income to the partners of the partnership who then must include their share of the distribution in their own individual income tax returns and pay tax at their marginal tax rates.

For example, you own a florist shop with Bob in a 50/50 partnership structure.

The flower shop earns $106,000 in income in 2025/26 and has deductible expenses of $30,000.

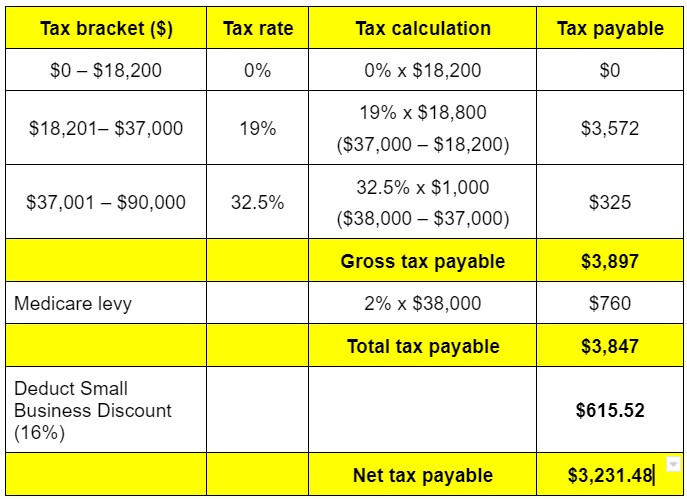

The net income of $76,000 will be distributed between you and Bob in equal proportions.

Tax is subsequently paid at each partner’s individual marginal tax rates.

With no other income or deductions, the taxable income will be $38,000 each. You and Bob will pay gross tax of $3,168 each, as shown opposite.

However, as a small business (operating as a sole trader, partnership or trust) with turnover less than $5 million, a small business income tax offset (credit) may apply. This discount is equal to 16% of the tax on your total net small business income up to a cap of $1,000 per individual. This reduces the tax for you and Bob by $506.88 each. Each partner would also be eligible for the low-income tax offset, which was discussed previously.