9 Estate Planning

Three-year rule

One option to reduce tax on an estate is to use the three-year rule.

This involves keeping assets within the estate for three years from date of death (and enjoy a separate tax-free threshold and marginal tax rates) rather than distributing them to high-earning individual/s but only if there is no beneficiary presently entitled to a distribution - and there is not a deliberate strategy to delay the winding up of the estate. After three years, any remaining income derived by the estate which is not distributed is taxed at the highest marginal tax rate.

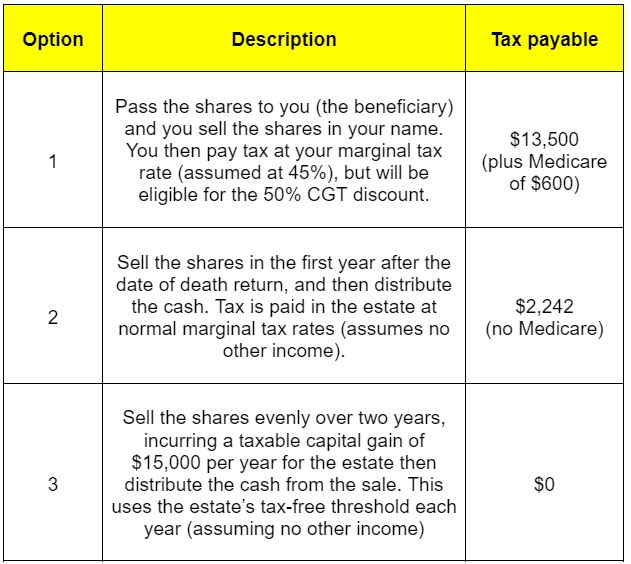

For example, let’s say an estate has one asset, being shares in Qantas which have been held for 10 years. This parcel of shares has capital gains of $60,000 if sold.

You're the only beneficiary. You earn $190,000pa and you would like cash instead of the shares.

Three options the executor of the estate has, including taxation consequences, are shown in the diagram opposite.